What is “chargeback insurance?”

“Chargeback insurance” is, first and foremost, a myth.

It does not exist.

The deceptive term “chargeback insurance” has been used in the fraud industry for years as a way to muddy the waters and imply there is some sort of “coverage” a merchant can purchase to hedge against the costs of chargebacks. These claims are missing the mark – insurance is purchased to mitigate potential risks; however, fraud is inevitable. It will occur today, tomorrow, and the day after.

Instead, fraud prevention providers are either accountable for their approved/declined decisions and carry the liability for chargeback costs and approval rates, or they are non-accountable and misleadingly offer a recommendation for which they are not financially liable.

Leveraging traditional insurance methods as a defense against fraud is not a sustainable approach. Unlike insurance, which is reactive, accountable fraud prevention involves continuous vigiliance and views risk as a shared responsibility. Imagine your insurance as a reimbursement when your house burns down. Wouldn’t you rather have a vigilant fire squad–an accountable fraud partner–who is ready to extinguish any smoke before it escalates and is completely liable if they are unable to put out the fire?

The term chargeback insurance remains in circulation because certain types of fraud providers want to obfuscate the fact that they are not accountable for their fraud decisions and have no liability for chargebacks that occur on their watch. These providers, “unaccountable” fraud protection vendors, would like merchants to believe that offloading chargeback liability is an expensive way for accountable partners to unnecessarily charge extra.

A few definitions related to the myth of chargeback insurance

What are chargebacks?

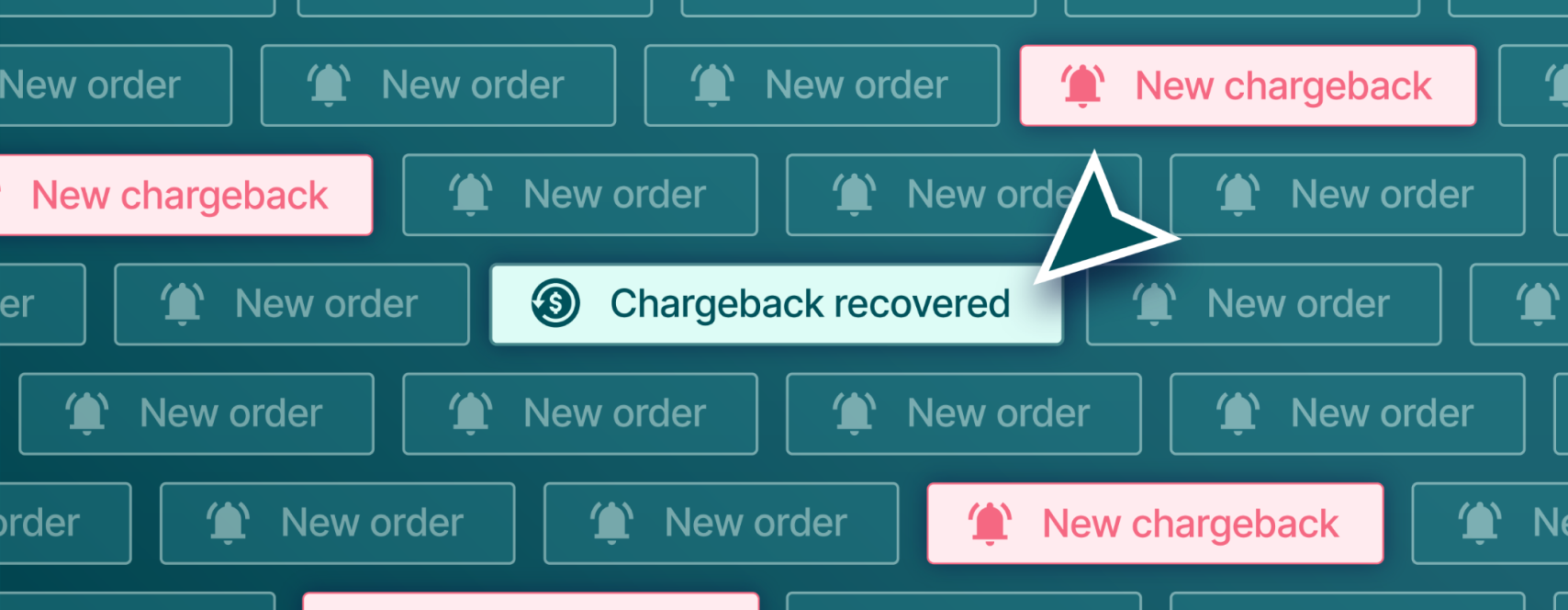

A chargeback occurs when a credit card owner notifies their card issuer that a transaction made to a merchant was unauthorized or otherwise problematic and requests a refund. The issuer then withdraws the money directly from the merchant’s account and returns it to the card owner’s account.

This process does not require the merchant’s consent and typically involves additional penalties to the merchant. Why? Because the merchant is responsible for making sure that card-not-present charges are valid and not fraudulent; if they accept a fraudulent payment, it’s on them.

The chargeback process is a consumer protection tool, but it can be abused, which is why merchants can dispute chargebacks they believe are invalid.

To protect themselves from fraud and its diverse costs, merchants work with fraud protection vendors, which may offer either “accountable” fraud protection or “non-accountable” fraud protection. Neither model involves chargeback insurance.

What is non-accountable fraud protection?

A non-accountable fraud vendor does not pay chargeback costs. Liability for chargebacks remains with the merchant. Fraud prevention vendors who do not guarantee their decisions are not accountable and thus have no financial burden or consequences for poor outcomes. These vendors frequently use a rules-based methodology, and they make the same revenue regardless of how many fraudulent transactions result in chargebacks.

What is accountable fraud protection?

An accountable fraud provider pays chargeback costs and has financial incentives aligned with the merchant’s. This alignment is assured by three characteristics of the accountable business model:

- An approval rate service level agreement sets a floor on the share of orders that the partner will approve. For instance, the partner commits to approving 98% of the merchant’s orders over the next two years.

- A chargeback guarantee shifts the costs of chargebacks with a fraud reason code from the merchant to the partner. This incentivises the partner to keep chargebacks low and make accurate order decisions.

- A performance-based fee structure rewards the fraud partner only for approved transactions and provides a disincentive to over-decline orders.

TicketNetwork achieves ROI with an accountable fraud partner

See how CFOs like TicketNetwork’s Chris Hummer are revolutionizing fraud management in their organizations.

Read case studyWhere can I get chargeback insurance?

Insurance is bought against potential risk, so in a world where fraud is absolutely certain, it is a misnomer. Ensure you have an accountable fraud partner who will offload inescapable chargeback costs while accurately approving/declining decisions to ensure cost predictability.

Reduce your chargeback costs to zero by working with an accountable vendor like Riskified.

Frequently asked questions

What is chargeback insurance?

The term chargeback “insurance” has been used in the fraud industry to misleadingly imply that merchants can purchase coverage to hedge against chargeback costs.

Why is the term “chargeback insurance” misleading?

Traditional insurance is purchased to mitigate potential risks, but fraud is inevitable, making insurance an unsustainable defense. Instead merchants can work with an accountable fraud partner like Riskified, who offloads inescapable chargeback costs and accurately approves or declines orders to ensure cost predictability.

Does a Chargeback Guarantee prevent chargebacks from happening?

A chargeback guarantee does not prevent chargebacks but shifts the financial liability for fraud-related chargebacks from the merchant to the fraud protection partner, incentivizing the partner to make accurate order decisions.

Learn about accountability-based fraud strategies in this guide for executive leaders.

This research with more than 300 chargeback managers reveals the size of the chargeback challenge, biggest pain points, and more.

Join Appriss Retail and Riskified experts as they uncover how fraud impacts omnichannel operations and how you can regain control

Request a personal demo

Learn how we boost ecommerce growth and reduce customer friction.

Contact us